I. April Building Materials Industry Prosperity Index

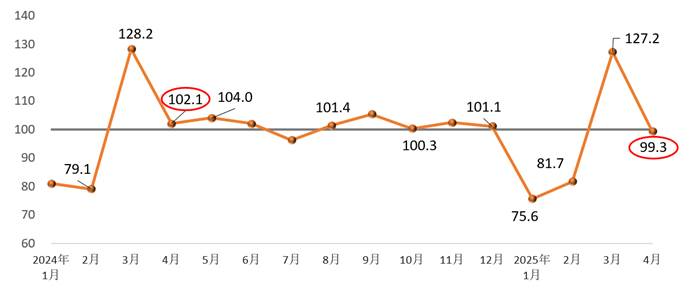

In April 2025, the Building Materials Prosperity Index (MPI) stood at 99.3 points, falling below the critical threshold and marking a 27.9-point decline compared to March. This places the industry in the contractionary zone, underperforming compared to the same period last year. Affected by both domestic and international market conditions—particularly the imposition of additional U.S. tariffs—production of building materials and downstream industrial products weakened, leading to a broad-based cooling in industry sentiment.

( Monthly Building Materials Industry Prosperity Index)

On the supply side, both the Building Materials Price Index and the Production Index remained below the threshold.

The Price Index was recorded at 99.7 points, up 0.4 points month-on-month, indicating a slight recovery.

The Production Index declined sharply by 28.4 points to 99.6 points, suggesting a weakening growth momentum and a return to the contraction zone.

Overall, prices for building materials showed a narrower decline and further consolidated a pattern of low-level stabilization, while production activity slowed compared to March.

On the demand side, the Investment Demand Index remained above the threshold, whereas both the Industrial Consumption Index and the International Trade Index stayed below it:

The Investment Demand Index was 100.1 points, although down 26.1 points from March, it still indicated a relatively stable outlook in line with last year's performance, reflecting steady conditions in the construction demand market.

The Industrial Consumption Index dropped to 96.5 points, a 33.6-point decline from the previous month, signaling weakened demand for construction-related materials in manufacturing, and falling short of last year's levels.

The International Trade Index came in at 97.7 points, down 47.7 points month-on-month, showing a notable reduction in foreign trade activity for building materials.

In summary, the overall demand side experienced a moderate pullback, with structural adjustments emerging. While investment demand remained stable, industrial consumption and external trade weakened.

II. MPI Influencing Factors and Market Outlook

Building materials prices continued their recovery and stabilization trend.

In April, among various sub-sectors of the industry, prices for wall materials, lightweight construction materials, insulation materials, lime and gypsum, dimension stone, mineral fibers, and composites rose on a month-on-month basis. Meanwhile, cement, clay and sand mining, dimension stone, mineral fibers, and composites saw their ex-factory prices rise year-on-year. Overall, the recovery trend in building materials prices that began in the second half of 2024 continued into April 2025.

Impact of U.S. tariffs became more pronounced.

Export orders for major product categories such as ceramic tiles, sanitary ceramics, stone, and glass—traditionally strong performers in the U.S. market—have come under direct pressure. In addition, the effects have cascaded upstream, impacting demand for automotive glass, fiberglass, and photovoltaic glass, which are linked to sectors like automobiles and solar cells. As a result, the Building Materials Industrial Consumption Index dropped into the contraction zone, with production indices for architectural glass, sanitary ceramics, and dimension stone also falling below the threshold.

Demand patterns are undergoing structural change, with infrastructure playing a stabilizing role.

Since the beginning of the year, the acceleration of major infrastructure projects, urban renewal initiatives, and government-backed “trade-in deals for building materials” have collectively provided a stabilizing foundation for market demand. Investment-side demand has remained steady, with cement, concrete, and cement products continuing to record production indices in the expansionary range in April. However, as U.S. tariff policies continue to evolve, demand from building materials–related manufacturing has become more volatile. This has added uncertainty and instability to foreign trade in building materials, affecting both industrial supply chains and downstream market expectations.

Annotations:

1. Building Materials Industry Prosperity Index (MPI)mainly monitors the operation trend of building materials industry and has a strong function of prediction and early warning. When MPI is higher than 100, it indicates that the operation of building materials industry is in the prosperity range, and when MPI is lower than 100, it indicates that in the recession range.

2. The prosperity index of building materials industry (MPI) judges the operation trend of building materials industry from the supply side and demand side. The supply side is divided into price index and production index. The demand side is divided into investment demand index, industrial consumption index and building materials international trade index according to the actual impact of the demand field on the building materials industry.

3. The price index of building materials industry reflects the change trend of ex-factory price of building materials industry. The ex-factory price does not include the expenses, product profits and taxes incurred in the circulation of building materials products. The ex-factory price is different from the market price, for the changes of the two will affect each other and there is a time lag. There may be inconsistent change trends in a certain period of time.

4. The industrial production index of building materials reflects the change trend of industrial production of building materials, excluding price changes.

5.Investment demand index, reflecting the change trend of investment market demand related to building materials.

6.The industrial consumption index reflects the changing trend of industrial consumption demand related to building materials. Industrial consumption includes not only the internal and inter industry consumption of building materials industry, but also the consumption of building materials products by downstream industries.

7.The international trade index of building materials reflects the changing trend of international trade in building materials, which is mainly composed of export indexes of building ceramics and sanitaryware, building technology glass, building stone, glass fiber and composite materials, non-metallic minerals and other industries.

Editor: Zhang Hanwen

Reviewer: Shen Yulu, Li Yuemei